The Importance of Understanding The Cash Conversion Cycle

Generally speaking, there are three sources of cash for a growing company. The most commonly discussed are equity and debt funding. Both come at a price. Debt comes with interest. Equity always comes with some sort of dilution of your own equity value in the company. The third source of cash is a more efficient use of the cash already in your business. Understanding where that cash is locked away and how to better access it will be how you’ll get at this, your cheapest source of growth capital.

There are many ways to understand the efficiency of cash flow management in your business. One way is to measure how quickly a company can convert cash on hand into even more cash on hand.

What Is the Cash Conversion Cycle?

The Cash Conversion Cycle (CCC) metric is an attempt to identify how cash moves through a company. More specifically, the calculation measures how much time is needed for a company to convert cash on hand into inventory and accounts payable, through sales and accounts receivable, and then back into cash. The lower the CCC, the faster a company is at turning an initial investment of cash into more cash.

What Are the Three Components of the Cash Conversion Cycle?

To measure the CCC, you need to know the:

- Days of Inventory Outstanding (DIO) : The average number of days a company holds inventory before it is sold. The lower this figure, the shorter cash is tied up in inventory. A DIO of 40 means that on average inventory stays in stock for 40 days before it is sold.

- Days Sales Outstanding (DSO) : The average number of days it takes to collect payment after a sale has been made. In retail markets, this should be zero because you collect payment at the point of sale, but in B2B businesses and with larger contracts, this may take longer.

- Days Payable Outstanding (DPO) : The average number of days it takes to process your own accounts payable. A DPO of 10 means, on average, it takes 10 days for your company or accounting department to pay suppliers.

Measuring The Cash Conversion Cycle (CCC)

Cash Conversion Cycle is measured with a simple formula:

DIO + DSO – DPO = CCC

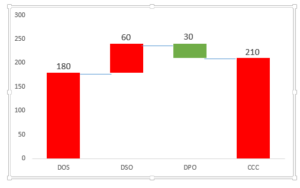

Here is an example of a business with the following data:

Days Inventory Outstanding: 180

Days Sales Outstanding: 60

Days Payables Outstanding: 30

CCC: 180 + 60 – 30 = 210 days

Let’s touch on each element:

DIO: Days Inventory Outstanding

(DIO = Inventory / Avg Daily COGS)

This metric measures how long it would take to sell through all of your inventory. It asks, “How long is cash tied up in inventory?” It is measured by taking the full value of inventory from the balance sheet and dividing it by your average daily cost of goods sold. It is recommended that you take at least 60-90 days of Cost of Goods Sold to determine a good average. Use even more if you have a seasonal business.

DSO: Days Sales Outstanding

(DSO = Accounts Receivable / Avg Daily Sales)

DSO measures how long it takes, on average, to collect from your customers once a sale is made. Of course, if you have only cash or credit card sales, your DSO will be zero. Smaller, or even negative (if you collect ahead of a sale) is good. Measure this by taking the full account receivable value from your balance sheet and dividing it by your average daily sales. Once again, use at least 60-90 days of history for your daily sales.

DPO: Days Payable Outstanding

(DPO = Accounts Payable / Avg Daily Expenses)

DPO measures simply how long your vendors allow you to wait to pay them. Your denominator here is the average daily expense and there are many ways to measure it. Some will argue whether payroll or cost of goods should be included. We recommend that you include in your average daily expenses all those expenses that you might be able to influence how long you take to pay them. With that perspective, most companies will include all expenses, except payroll. This is because all of your expenses, with the exception of payroll as a last resort, can likely be sped up or down as needed to assist with managing cash.

Once each metric is measured, they can be combined into the CCC which then indicates the company’s ability to employ short-term assets and liabilities to generate cash. It measures the liquidity risk you take when you put cash into growth strategies. It demonstrates how long it will take until you see a return.

Analyzing The Cash Conversion Cycle (CCC)

Investors often use this metric to compare close competitors, as a low CCC signifies an opportunity to improve cash generation. But for those wanting to use this metric internally, there are two things to learn from an analysis of your CCC.

First, as mentioned, improving the efficiency of capital already in your business is your cheapest source of additional capital to grow your business. It doesn’t cost you any interest or equity dilution. A study of the overall CCC and its individual components will help you understand where you can streamline. For instance, you may dig deeper into your Days Inventory Outstanding and determine to move away from some slower moving products. Whether or not those products are profitable, you may decide you want access to that cash to grow the business more efficiently elsewhere.

Two, if you measure the CCC over time (and you can measure backward by simply looking at historical data) by graphing CCC and its component parts on a trend line, you can learn whether you’re improving or not in recent months. This is particularly helpful to catch problems early as they arise in your business. These patterns over time are very telling.

What Does It Mean If the CCC Is Negative?

A negative CCC means that it takes longer to pay your accounts payable (bills, invoices, suppliers) than it takes to sell your inventory and collect your money.

CCC is only a metric. There is no such thing as a good or bad score. You must determine within your company the importance of the cash conversion cycle.

Paying close attention to cash management by measuring how efficient you are as an organization is just the first step to unlocking your cheapest source of capital. Once you’ve gained understanding you can begin to lay out a plan for improvement. Below are two additional sources of good information on measuring and analyzing your cash conversion metric.

Read more: Cash Conversion Cycle – CCC (AMZN)